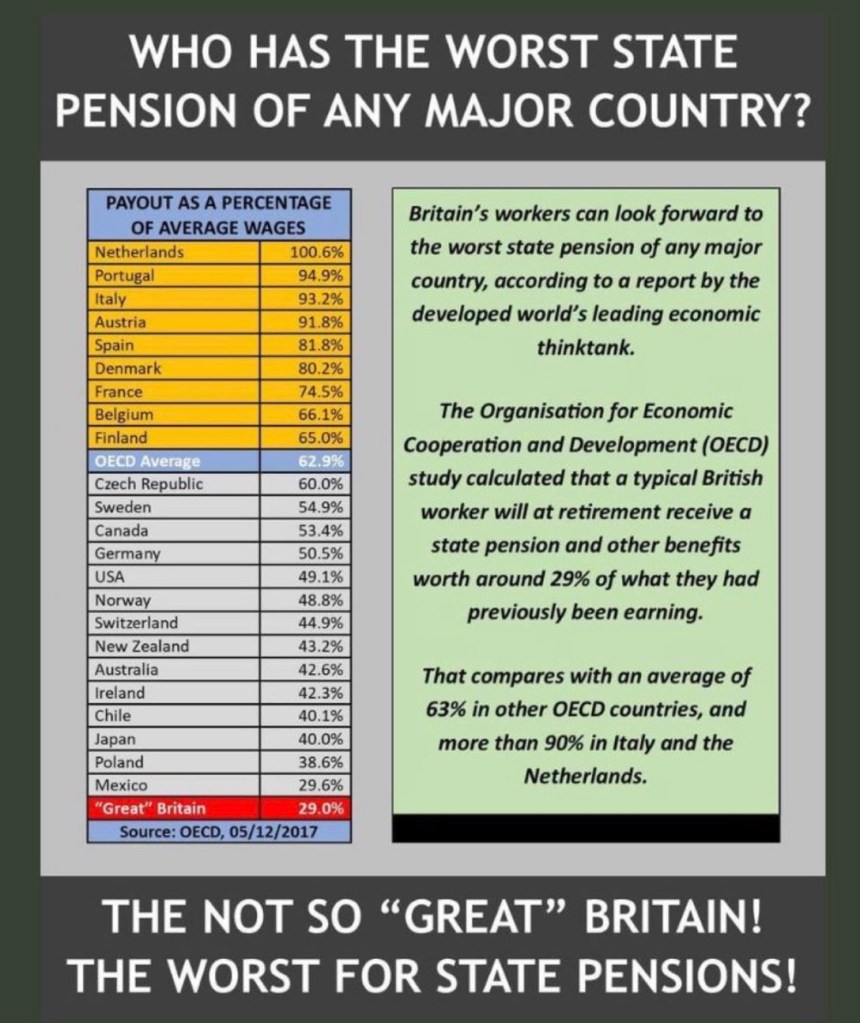

The above table is accurate, but a tad misleading. This is because many British pensioners of my immediate post war generation enjoy workplace pensions from an established Defined Benefit (DB) scheme. These schemes, which first appeared in the late 1940s, give employees on retirement a guaranteed pension related to their final salary and are index-linked.

Millions of us have DB pensions to which can of course be added our State Pension. Elsewhere in the world there are also workplace pensions and for a fair comparison to be made we should show a table which adds average workplace pension to state pension to get total pension.

Ex Pensions Minister Ros Altmann told me “It is true that the UK pays the lowest state pension in the developed world. It has always has. Low state pension was supposed to be supplemented by a private [workplace] Pension top up.”

Ros makes the point that from a Government perspective the tax benefits of workplace pensions are a cost to the exchequer that needs to be factored in “The tax reliefs given to private pensions cost huge sums but are meant to help ensure people have enough to live on in later life.” In effect there is a choice between giving tax relief to workplace pensions and a lower State pension or, in theory, reducing the tax benefit but increasing the State pension to compensate.

The Pension situation of my generation is far superior to that of many younger people who when they retire in many cases will have far lower and far less inflation-proofed workplace pensions. As Ros puts it “Sadly private pensions are not evenly spread and many pensioners have no private pension.” This is a snapshot of the current position and one that will get worse in the decades ahead. The reason for this changed situation is that most employers no longer offer new recruits DB scheme pensions even where they maintain “heritage” Pension Funds to honour their obligations to the retired. These schemes have for some time mostly been closed to new entrants.

I am writing here about mostly private sector workplace pensions. In the public sector DB schemes (or equivalent pension arrangements) do provide employees with significantly better prospects of final salary linked (average salary in some cases) and an inflation proofed retirement income. I have covered this subject in a video which you can watch here.